Subscribe to continue reading

Subscribe to get access to the rest of this post and other subscriber-only content.

Subscribe to get access to the rest of this post and other subscriber-only content.

Subscribe to get access to the rest of this post and other subscriber-only content.

Subscribe to get access to the rest of this post and other subscriber-only content.

Subscribe to get access to the rest of this post and other subscriber-only content.

Subscribe to get access to the rest of this post and other subscriber-only content.

It’s good to see the CMA continuing to adapt its merger control processes with a view to making them work even better than they already do.

I’m hoping that the new processes will be a great success for UK consumers.

Most commentators seem to think, however, that the onus is solely on the CMA to make the system work better than before.

Really?

From what I’ve seen many of the problems experienced with the current system have occurred because of

Indeed, some of the problems encountered at Phase 2 go right back to choices made earlier in the merger process.

Through the changes it is making the CMA is providing different opportunities for interested parties to engage better with the investigation process.

It seems to me that an awful lot is riding on how well some companies and their advisers will use the changes being made and improve how they interact with the process more generally.

The new system won’t greatly benefit UK consumers unless some of those participants change too.

As the song once put it – ‘It takes two to tango”

So here’s a key question for companies and advisers as they approach future investigations under the revised investigation process:

What specifically will you do differently to make the new arrangements work well?

And how will you go about reviewing and challenging your previous way of doing things?

An investor tells me with certainty that, if the high profile deal in which he is interested happens, the CMA will definitely clear it.

“They (the acquirer) wouldn’t go ahead if they weren’t absolutely sure they could get it through”, he insists.

It’s a view that I’ve heard many times during my investor briefings on mergers from supermarkets to video games.

It’s a bold claim.

Which is why – when it crops up – I usually find myself asking briefing participants the following:

What would have to be true for this to be the case?

At which point participants to the discussion tend quickly to alight on three big assumptions:

1. That the acquirer has prepared perfectly for all eventualities

2. That none of the eventualities results in any risk whatsoever that the CMA will find competition problems.

3. That this acquirer would only proceed with absolute certainty of outcome.

When that happens discussion often then turns to how frequently these assumptions have held in similar past cases.

Quite a lot is known about that, under all three headings.

And when that is discussed, guess what tends to happen next.

I’ve been very struck over the years by how differently companies prepare for CMA hearings during merger investigations.

Hearings are an important feature in many merger investigations, providing an opportunity for the merging firms, rivals and other interested parties to make their case.

Some hearings are turning points in a case.

Some are wasted opportunities.

Much depends on how hard the organisations involved think (or don’t think) about the objectives they set themselves.

Some prepare to dial up the rhetoric.

Some prepare to move the dial.

So, for all those with CMA hearings in view here’s a key question to start with…..

What are you really preparing for ?

There’s been a big overall decline in the percentage of CMA cases cleared unconditionally (at Phase 1 or Phase 2)* in recent years.

It’s been much commented on and interpreted.

But it’s not quite what it seems when you look behind the headline numbers.There are very different patterns when looked at by case type.

![]()

In fact, arithmetically at least, the aggregate change is accounted for by just one type of case.

Here’s the overall pattern for 2019 and 2020 cases, with the size of the different elements proportional to the number of outcomes in each category – where

Source: Adrian Payne analysis of published CMA decisions

It illustrates how important it can be to look behind the aggregate numbers when considering past or potential case outcomes and when interpreting ‘trends’ in the aggregrate numbers.

In one of my next Merger Insight briefings I’m going to be discussing the reasons behind these patterns and what they mean for companies planning mergers.

—————————————————————————————

(* Percentage of publically-investigated cases. Takes no account of cases the CMA chooses not to investigate publically, on which no meaningful data are published.)

———————————————————————————————

Thank you for reading. If you found the article informative please feel free to share it using the sharing buttons nearby.

Surprise, surprise

Why are so many companies surprised to find their mergers investigated by the CMA?

It’s partly down to the elasticity with which the CMA exercises its ‘share of supply’ jurisdictional test.

Over the past year of two I have featured some persuasive articles on this in my UK Merger Spotlight.

Perspective

It’s important, however, to keep a sense of perspective:

The share of cases examined under the share of supply test is well towards its CMA low, as the diagram here shows.

Growing Unease

Maybe there are other reasons why unease among merging companies and their advisers has been growing about ‘share of supply’ cases?

Here are three:

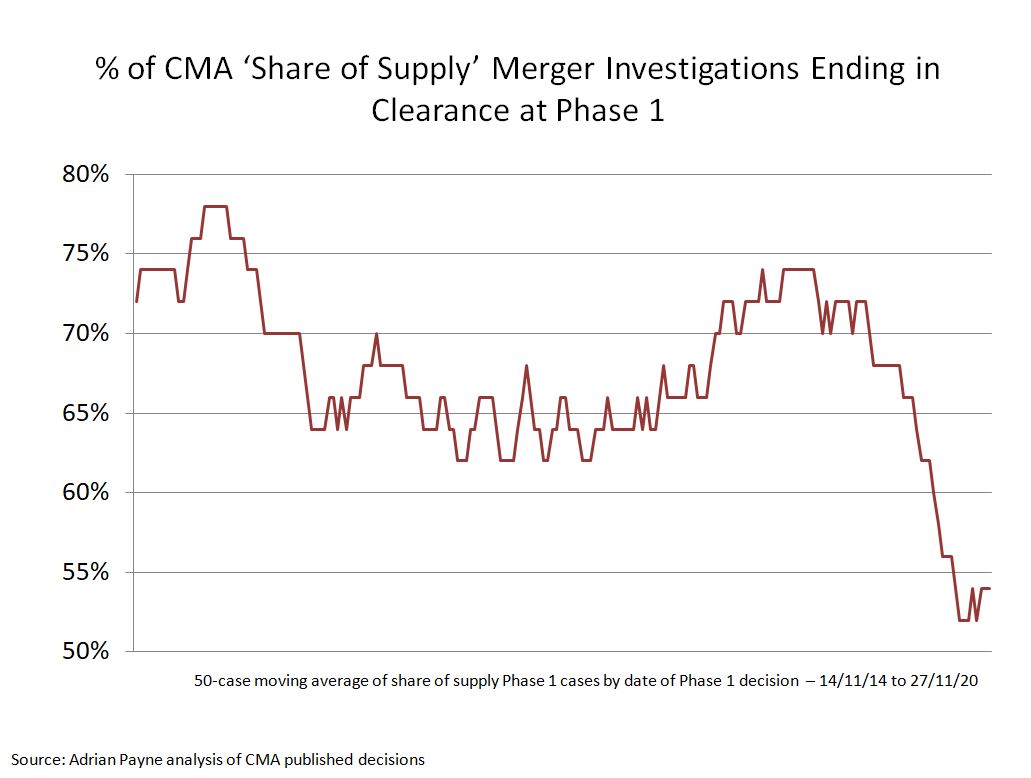

As the following diagram shows, since mid-2019 the proportion of ‘share of supply’ cases cleared at Phase 1 has nose-dived.

By contrast, the proportion of clearances among cases investigated under the CMA’s £70m turnover test has continued to climb – up to a CMA record of nearly 75%.

2. More referrals of ‘share of supply’ cases for in-depth Phase 2 investigation

The proportion of ‘share of supply’ cases referred for a Phase 2 investigation during the second half of the CMA’s case portfolio has been double what it was in the first half. (Meanwhile the proportion for ‘turnover test’ cases has stayed about the same).

3. Worsening outcomes at Phase 2 for ‘share of supply’ cases

The proportion of ‘share of supply’ cases cleared at Phase 2 has also dropped sharply between the two periods (though here there has also been a smaller but significant drop in the proportion of turnover test cases cleared at Phase 2).

In 2020, these three developments have culminated in

So What?

1. Increases pressure for change

Well, for a start, the ‘share of supply’ case outcomes may explain some of the current criticism of the UK’s ‘voluntary’ notification regime.

Some would like the UK to move to a more ‘mandatory’ notification regime, with no share of supply test or with a share test that gives the CMA much less discretion. (It would, of course, be ridiculous to think that some such calls might also have anything to do with views on Brexit !)

2. Demonstrates the contribution of the ‘share of supply’ test

Second, the figures bring home how important the ‘share of supply’ test has been and continues to be to the UK merger control regime.

There is considerable onus therefore on those who advocate change to show how the contribution that the ‘share of supply’ test has made to the protection of UK consumers can be preserved or enhanced in any new system without adding unduly to the burden on merging parties or the taxpayer.

3. Provides important lessons for merging firms

And finally, for companies who may be considering merger in coming months the figures show how important it will be to take ‘share of supply’ test considerations fully into account in assessing UK merger control risk.

On this point it’s worth noting too that over a third of ‘share of supply’ cases examined so far this year were selected for investigation by the mergers intelligence function (a much higher proportion than for turnover test cases).

Especially in the new post-Brexit environment it is important for companies – even those with limited activities in the UK – to consider more carefully whether the CMA might take an interest in their deal, even where potential grounds for that interest might not be immediately obvious.

If that happens maybe the ‘share of supply’ test will spring fewer surprises in 2021 ?

In January 2021 I will be running a Merger Insight briefing discussing:

”The Extra Questions Merging Companies Need To Ask About The UK Share Of Supply Test.”

Details will be posted here. Do drop me a line if you would like to register interest now.

Thank you for reading this article — I hope you enjoyed it. Please do share it far and wide — there are handy sharing buttons nearby.