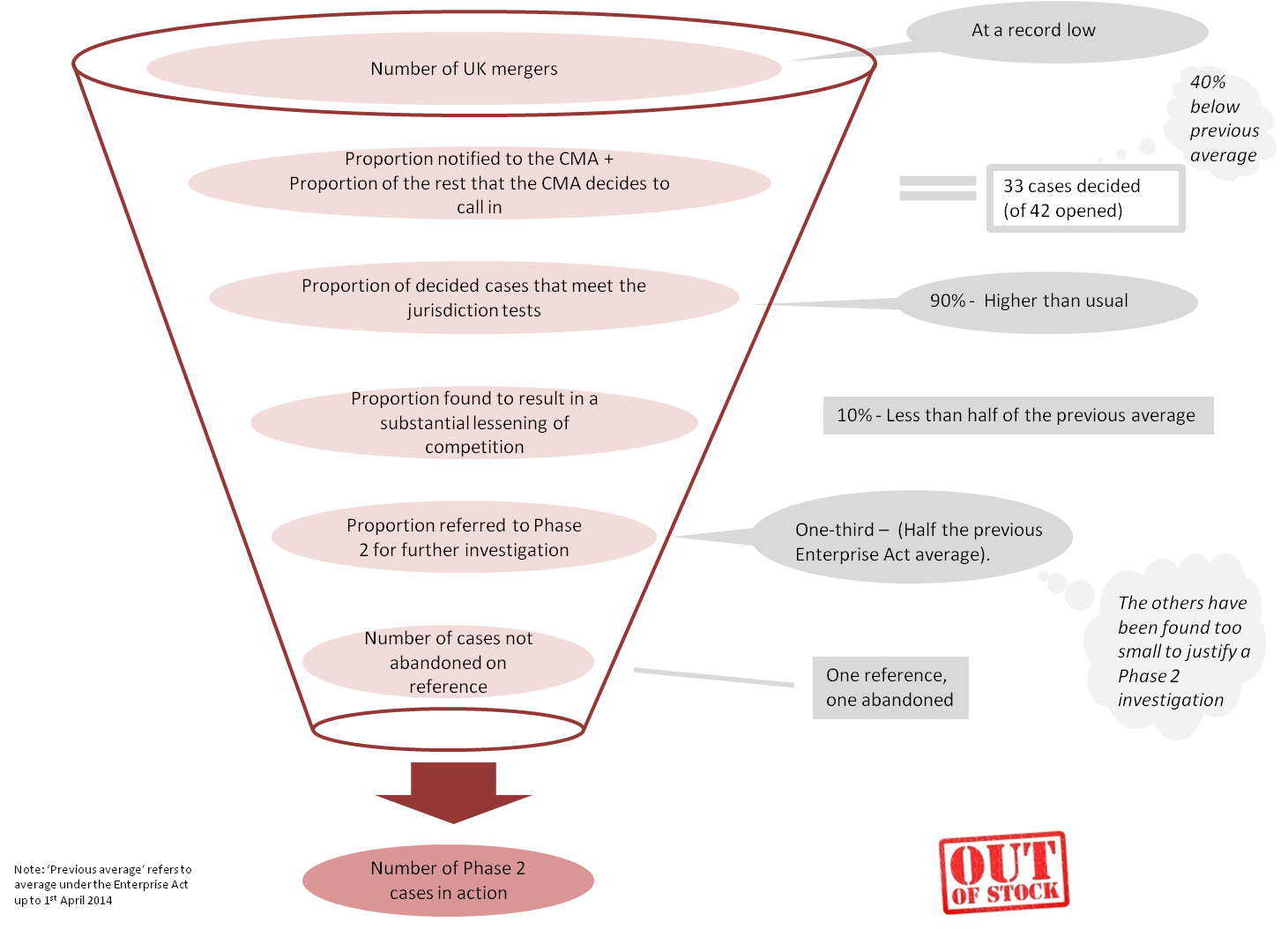

Just when some companies thought it was becoming safer to merge the Competition and Markets Authority has found competition problems with five mergers …..

Just when some companies thought it was becoming safer to merge the Competition and Markets Authority has found competition problems with five mergers …..

.. in just six weeks

(These relate to Phase 1 merger cases requiring further Phase 2 investigation, or undertakings to resolve the problems, for which decisions were announced between December 1st 2014 and January 15th 2015)

This after the CMA identified just four problematic deals at Phase 1 during the whole of 2014 up to the beginning of December (excluding cases deemed too small to justify a Phase 2 investigation).

What should companies currently contemplating difficult deals make of this recent bunch of five?

As always with short sequences of merger decisions it is vital to take a long view and to avoid the temptation to read too much into too few decisions.

So what does the long view look like?

The history of Phase 1 decisions under the 10+ years of the Enterprise Act helps put things in perspective.

In actual fact the UK merger authorities have delivered several speedy bunches of five over the years….2006, 2011 and 2012 each contained six-week periods in which five mergers were found to raise competition concerns at Phase 1.

And those episodes are by no means the record.

In early 2005 there was a similar period when seven deals fell foul of the then-OFT’s decision-makers. And later that same year eight deals were found to be problems in just over a month.

What is more, this number of five-plus/six-week bunches over the years is more or less exactly what one would expect given the average number of cases each year and the average probability of a case giving rise to an adverse competition finding.

And, not to forget that the latest Christmas/New Year decision-making flurry followed an influx of new cases in October that numbered well above average. Perfect timing for a bumper seasonal delivery of merger decisions.

So while it is true that a bunch of fives from the UK’s merger authorities hasn’t happened that often, it is also the case that it has not been that unusual either.

No need for companies to worry unduly yet about the latest bunch of fives.

————————————————————————————————–

© Adrian Payne 2015